IFRS 16 (Leases) – The impact on business valuations

Henri Heinola, Senior Valuation Consultant at Globalview Advisors shares insights on the impact of IFRS 16 has on business valuations and outlines what accountants need to be aware of.

Henri Heinola, Senior Valuation Consultant at Globalview Advisors shares insights on the impact of IFRS 16 has on business valuations and outlines what accountants need to be aware of.

IFRS 16 replaces IAS 17 and is effective for annual reporting periods beginning on or after 1 January 2019. IFRS 16 eliminates the classification of leases as either operating leases or finance leases for a lessee. Instead all leases are treated in a similar way to finance leases under IAS 17. IFRS 16 will have a significant impact on companies that have relied on off-balance sheet financing in the form of operating leases, particularly in the airline, retail, transportation, telecommunication, and energy sectors.

Under IFRS 16 a lessee is required to recognise:

The impact on the balance sheet will be twofold, the recognition of a right-of-use asset and a lease liability. As a result, companies that have previously had significant off-balance sheet leases will now show higher assets and higher liabilities.

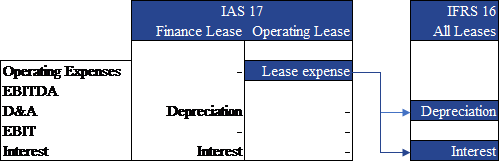

IFRS 16 impacts the lessee’s P&L where they have previously classified leases as operating leases. The lease expense recognised under IAS 17 will now be recognised as depreciation of the right-of-use asset to be recognised on the balance sheet as well as an interest expense. As a result of implementing IFRS 16, operating expenses will be lower, interest expense will be higher, and EBITDA and EBIT will be higher.

The total cashflows of a company will not change as a result of implementing IFRS 16. However, IFRS 16 is expected to impact the classification of cash flows generated through operating and financing activities. Compared to IAS 17, cash from operating activities is expected to increase under IFRS 16 as cash outflows related to operating leases will no longer be included within cash from operating activities. The increase in cash from operating activities will be offset by a decrease in cash from financing activities as cash outflows related to principal repayments and interest (interest can be recognised under financing activities under IFRS) on lease liabilities will be recognised within cash from financing activities.

As a result of IFRS 16 the NPV of free cashflows to the firm (“FCFF”) are expected to be higher resulting in a higher Enterprise Value (“EV”). The higher NPV of FCFF are a result of a higher EBITDA and lower WACC absent any adjustments in market pricing metrics observed. The WACC is expected to be lower as a result of a higher D/E mix in the capital structure of peer group companies used to determine the target capital structure. Although the Enterprise Value will increase, equity value should remain unchanged i.e. theoretically the increase in enterprise value should be offset by the increase in net debt.

Prior to IFRS 16 all lease expenses for operating leases were captured in operating expenses and hence, included in the determination of EBITDA. Consequently, lease expenses were consistently incorporated into the free cashflow forecasts of the company. However, post IFRS 16 there will no longer be an operating expense for leases, but rather a depreciation (non-cash expense) and interest expense which are not captured within EBITDA. Additionally, the increase in net debt only captures the present value of lease obligations for the remainder of the lease term(s) i.e. the P.V. of lease liability does not capture the future cash outflows reflecting the renewal of the leases in future periods (conceptually, into perpetuity from a valuation perspective). When using the DCF method, care should be taken to ensure cash outflows related to the continuation of the leases into perpetuity are considered in valuing the business.

A further consideration in using the DCF method relates to capex and depreciation. Prior to IFRS 16, unless a company was forecasted to have significant growth capex, a common assumption used by valuers and analysts was that capex equals depreciation. However, post IFRS 16 this simplifying assumption will no longer be valid. Depreciation related to leases should not be offset by capex as this is already reflected in the present value of lease obligations within net debt. As a result, careful consideration needs to be given to capex when performing company valuations after the implementation of IFRS 16.

Valuation of companies using the GCM is also affected by IFRS 16. Multiples based on Enterprise Value such as EV/EBITDA will be affected as EV and EBITDA will both be higher. EV increases as a result of recognising the P.V. of lease liabilities and EBITDA increases due to the removal of the lease expense. In most cases, EV/EBITDA multiple is expected to be lower post IFRS 16 as the relative impact of IFRS 16 on EV is expected to be lower compared to the impact on EBITDA.

The relative magnitude of change in the Enterprise Value and EBITDA post IFRS 16 will vary between companies as the present value of lease liabilities and the value of the right-of-use asset depend on length of the lease(s) and interest rates/incremental borrowing costs (used as discount rate in computing P.V. of lease liabilities) which will vary amongst companies. The longer the lease period and the lower the discount rate used to compute present value of lease liabilities, the higher the value of the lease liability and the right-of use asset. Longer lease periods also result in a lower depreciation expense compared to an identical lease for a shorter period.

In valuing companies in 2019, consideration must be given on whether to rely on FY2018/Latest Twelve Month (“LTM”) multiples. This is because LTM multiples will not be comparable to FY2019/Next Twelve Month (“NTM”) multiples for companies which have decided to apply IFRS 16 using the modified retrospective approach as LTM multiples will not include the impact of IFRS 16 but NTM multiples will. Consequently, it is important for valuers or analysts to determine whether guideline companies have applied IFRS 16 using the modified retrospective or the full retrospective approach.

Commonly valuation practitioners analyse guideline transactions within the industry during relevant years prior to the valuation date to compile a reasonable group of guideline transactions. As a result of IFRS 16 changes, the observed multiples in historical transactions (prior to IFRS 16) will not be comparable to post IFRS 16 profitability measures such as EBITDA or EBIT. It could take several years before a sufficient number of post IFRS 16 transactions have occurred in various sectors to enable valuers to utilise the GTM in valuing companies using traditional enterprise value-based multiples. However, valuers/analysts using the GTM might start applying multiples (based on pre IFRS 16 profitability measures such as EBITDA) to post IFRS 16 profitability measures of the subject company such as “EBITDAal” (EBITDA after leases i.e. including lease related depreciation and interest expense).

Adoption of IFRS 16 results in various areas which must be carefully considered especially when valuing companies using DCF, GTM and GCM valuation methods.

About the author:

Henri Heinola is Senior Valuation Consultant at Globalview Advisors, an independent financial advisory firm focused on intangible asset and business valuations for financial reporting and tax purposes.