What did we learn from the FRC's latest audit quality review?

The Financial Reporting Council’s Annual Review of Audit Quality for 2024, released on July 30, 2024, paints a picture of an audit landscape in flux – a tale of two tiers that both inspires confidence and raises alarm bells.

At first glance, the headlines are encouraging. A robust 74% of audits inspected were deemed good or requiring only limited improvements. The FTSE 350, the crown jewels of UK business, saw their audit quality climb from 81% to an impressive 87%. For those keeping score internationally, the UK’s performance for its largest listed businesses is turning heads.

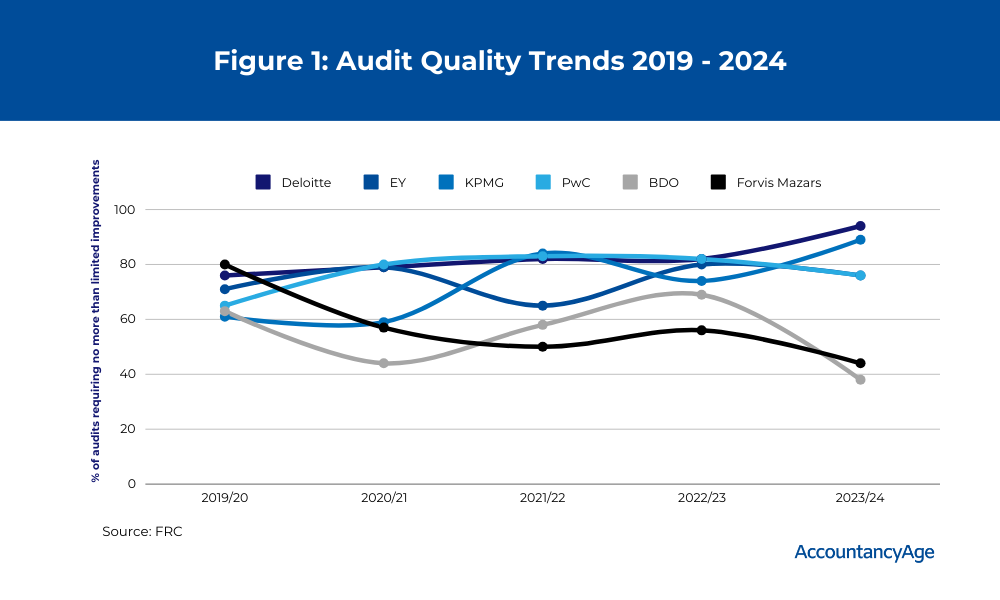

But beneath this veneer of progress lies a story of divergence. The “Big Four” – Deloitte, EY, KPMG, and PwC – have been on a five-year journey of improvement, with Deloitte leading the pack at a stellar 94% success rate. Yet, as these giants stride forward, their Tier 1 peers, BDO and Forvis Mazars, find themselves stumbling. BDO’s performance plummeted from 69% to 38%, while Forvis Mazars slipped from 56% to 44%.

This widening gap within the Tier 1 ranks is more than just numbers on a page. It speaks to the heart of the audit profession’s challenges: maintaining consistent quality across a diverse market, adapting to technological changes, attracting top talent, and balancing public interest with commercial pressures.

“The FRC welcomes the audit quality improvement at the largest four audit firms… However, BDO and Forvis Mazars’ performance has fallen significantly below our expectations,” says Sarah Rapson, the FRC’s Executive Director of Supervision.

In this analysis, we’ll delve deep into the performance of each Tier 1 firm uncovering the stories behind the numbers.

Deloitte has demonstrated exceptional performance in the 2024 FRC review, with 94% of its audits categorized as good or requiring only limited improvements. This represents a significant improvement from 82% in the previous year, placing Deloitte at the forefront of audit quality among Tier 1 firms. Notably, 100% of FTSE 350 audits reviewed achieved this high standard, up from 82% in the prior year. Only one audit out of the 17 inspected was found to require significant improvements.

The firm’s performance shows a consistent upward trend over the past five years, moving from 76% in 2019/20 to the current 94%. This positive trajectory demonstrates Deloitte’s commitment to continuous improvement and its ability to adapt to evolving regulatory expectations. The firm has shown particular progress in FTSE 350 audits, achieving a perfect score in the current review.

The FRC report highlighted several areas of good practice in Deloitte’s audits:

While Deloitte’s overall performance was strong, the FRC identified two key areas for improvement:

These areas, while not pervasive, indicate opportunities for Deloitte to further refine its audit approach in complex, judgmental areas.

Deloitte has responded positively to the FRC’s findings. The firm has committed to:

Deloitte has successfully implemented ISQM (UK) 1 and completed its first annual evaluation. While the firm’s efforts in this area are commendable, the FRC noted some areas for improvement, including strengthening certain monitoring processes and enhancing the documentation of the annual evaluation process. The firm has already begun the iterative process of improving and refining its SoQM in response to the FRC’s feedback.

Challenges and Innovations

Deloitte faces the ongoing challenge of maintaining its high standards across a large and diverse audit portfolio. The firm is addressing this through a multi-faceted approach.

At the forefront is continued investment in audit quality initiatives, with a particular focus on developing its audit culture. This is complemented by the expansion of its Continuous Improvement Group’s scope of work, which aims to identify and implement best practices across the firm.

Deloitte is also refining its Single Quality Plan (SQP) on an ongoing basis, using it as a tool to drive measurable improvements in audit quality. Recognizing the changing landscape of audit delivery, the firm is adapting to the increased use of offshore delivery centers by evolving its quality control processes to ensure consistent quality across all locations.

Additionally, Deloitte is in the process of implementing new audit software, a significant undertaking that will be rolled out over the next three years. This technological upgrade demonstrates the firm’s commitment to leveraging advanced tools to enhance audit efficiency and effectiveness.

Collectively, these initiatives showcase Deloitte’s proactive stance in addressing emerging challenges and its dedication to maintaining its position at the forefront of audit quality in an ever-evolving professional landscape.

Read Deloitte’s full report here: Deloitte_LLP_Audit_Quality_Inspection_and_Supervision_Report_2024

EY’s performance in the 2024 FRC review shows a consistent level of quality, with 76% of its audits categorized as good or requiring only limited improvements. This is similar to the previous year’s result of 80%. Notably, none of the audits inspected were found to require significant improvements, marking the fourth consecutive year of achieving this standard.

The firm’s performance over the past five years shows a relatively stable trend, with results ranging from 65% to 80% of audits requiring no more than limited improvements. While there’s been no dramatic improvement, EY has maintained a consistently solid performance. However, the results for FTSE 350 audits showed a decline, with only 50% assessed as good or requiring limited improvements, down from 89% in the previous year.

The FRC report highlighted several areas of good practice in EY’s audits:

The FRC identified three key areas for improvement in EY’s audit quality: testing of revenue and journals, audit of impairment and deferred tax assets, and audit of carrying value of investments in subsidiary undertakings.

Recurring issues were noted in revenue and journal testing, including insufficient validation of third-party revenue reports and inadequate journal testing procedures. Weaknesses were found in the evaluation and challenge of cash flow forecasts and other key assumptions related to impairment and deferred tax assets.

Additionally, material misstatements were not identified in the carrying value of parent company investments in two audits. In response to these findings, EY has committed to several actions. The firm plans to issue bespoke coaching packs for journals, revenue, and impairment, and deliver targeted training on key areas such as prospective financial information and recoverability of investments in subsidiaries.

EY is also enhancing existing standardized work programmes, particularly for impairment assessments, and developing good practice examples of documentation.

Furthermore, the firm is mandating additional specialist involvement in certain complex areas. These actions demonstrate EY’s positive response to the FRC’s recommendations and its commitment to improving audit quality in these identified areas.

As with all large audit firms, EY faces the challenge of maintaining consistency across a diverse portfolio of audits.

The firm must also navigate the increasing complexity of financial reporting, the integration of new technologies like AI, and the ongoing need to attract and retain top talent. EY’s steady improvement suggests success in managing these challenges, though the gap with the top performers indicates room for further innovation.

Read EY’s full report here: Ernst__Young_LLP_Audit_Quality_Inspection_and_Supervision_Report_2024

KPMG: A Strong Comeback Story

KPMG: A Strong Comeback StoryKPMG has demonstrated notable improvement in the 2024 FRC review, with 89% of its audits categorized as good or requiring only limited improvements. This represents a significant increase from 74% in the previous year. Of the 19 audits inspected, only two were assessed as requiring improvements, with none requiring significant improvements.

The firm’s performance shows a strong positive trend over the past five years, moving from 61% in 2019/20 to the current 89%. This trajectory demonstrates KPMG’s commitment to continuous improvement and its ability to effectively implement quality enhancement initiatives. The firm has shown particular progress in FTSE 350 audits, with 88% (7 out of 8) achieving the highest standard.

KPMG showed effective challenge of management across multiple audit areas, including impairment testing, property valuations, revenue recognition, and going concern assessments. The firm demonstrated robust impairment assessments, particularly in the use of third-party research and benchmarking to corroborate management’s assumptions.

KPMG’s effective involvement of specialists in complex areas was noted, with examples in insurance provisioning, pension scheme obligations, fair value measurements, and IT assessments. The firm exhibited strong group audit oversight, implementing a staged approach to reviewing component auditors’ work that allowed timely evaluation and response to emerging issues.

KPMG also demonstrated high-quality controls testing, with comprehensive assessment of the operating effectiveness of cost controls. Additionally, the firm’s Engagement Quality Control Reviews (EQCR) were commended for providing strong challenge over significant risk areas, clearly enhancing audit quality.

The FRC identified two key areas for improvement:

KPMG has implemented ISQM (UK) 1 and completed its first annual evaluation. The firm demonstrated good practices in risk identification and response design. However, improvements are needed in monitoring processes and the assessment of deficiencies.

KPMG faces the ongoing challenge of sustaining its improved performance and ensuring consistent high-quality audits across its portfolio. To address these challenges, the firm has implemented a comprehensive strategy. Central to this is the Single Quality Plan (SQP), which drives measurable improvements in audit quality and is at the forefront of the firm’s regulatory strategy.

KPMG is focusing on changing the shape of audits to reduce work intensity in periods close to signing, aiming to improve both audit quality and team wellbeing. The firm is investing in technology to enable better monitoring of engagements, providing enhanced support to audit teams. KPMG has also significantly enhanced its root cause analysis process, increasing the extent and breadth of reviews to better understand and address quality issues.

The firm is improving its project management and resource allocation, including the introduction of a flexible resource pool to respond more effectively to changing demands within the business. Additionally, KPMG is placing emphasis on its culture programme, focusing on recognizing and responding to biases that can occur in audits, and strengthening its second line processes to challenge areas where bias may have occurred.

Read KPMG’s full report: KPMG_LLP_Audit_Quality_Inspection_and_Supervision_Report_2024

PwC has demonstrated strong performance in the 2024 FRC review, with 76% of its audits categorized as good or requiring only limited improvements. This result is largely consistent with recent years, showing sustained high-quality audits. Notably, 100% of FTSE 350 audits reviewed achieved this high standard, an improvement from the previous year.

The firm’s performance over the past five years shows a relatively stable trend, with results ranging from 65% to 83% of audits requiring no more than limited improvements. While there’s been no dramatic improvement recently, PwC has maintained a consistently solid performance, particularly in FTSE 350 audits.

The FRC report highlighted several areas of good practice in PwC’s audits. These include robust impairment assessments, where the firm effectively used third-party data and industry experts to challenge management’s assumptions.

PwC also demonstrated comprehensive risk assessment procedures and effective group audit planning, including detailed planning workshops for component auditors. The firm showed strong challenge of management through independent modelling and benchmarking, particularly in areas such as expected credit loss models and pension valuations.

Effective group audit oversight was noted, with thorough assessment of component auditors’ work. Additionally, PwC exhibited robust going concern procedures, including convening technical panels and delaying signing when necessary. The firm’s high-quality reporting to Audit Committees was also commended, with reports including challenges encountered in the audit and how key findings from FRC public reports were addressed.

The FRC identified three key areas for improvement:

PwC has implemented ISQM (UK) 1 and completed its first annual evaluation. The firm demonstrated good practices in risk assessment and response design. However, improvements are needed in monitoring procedures and the assessment of other sources of findings.

PwC faces ongoing challenges in maintaining consistent high quality across its large audit portfolio. To address these challenges, the firm has implemented a multi-faceted approach. PwC continues to prioritise audit quality through its Audit Quality Plan and Single Quality Plan, which are aligned with the firm’s overall audit strategy.

A key focus is on embedding and reinforcing ethical and audit behaviours, aiming to cultivate a culture centered on achieving high-quality audits. The firm is also working on maintaining a balance between the demand for audit services and the supply of available auditors, recognizing the importance of appropriate resourcing. PwC is improving its project management approach, particularly in how audits are phased, including agreement of timely deliverables with entity management.

The firm is supporting audit teams through the transition period for new standards, ensuring they are well-equipped to handle evolving regulatory requirements. Additionally, PwC is placing continued focus on future talent development, including coaching initiatives and development programmes, to ensure a skilled and motivated workforce capable of delivering high-quality audits.

Read PwC’s full report here: PricewaterhouseCoopers_LLP_Audit_Quality_Inspection_and_Supervision_Report_2024

Performance Overview BDO’s performance in the 2024 FRC review has raised serious concerns, with only 38% of its audits categorized as good or requiring limited improvements. This represents a significant decline from 69% in the previous year, placing BDO in a precarious position among Tier 1 firms.

The firm’s performance shows a sharp negative trend, reversing the more encouraging trajectory seen since 2020/21. This decline is particularly worrying given BDO’s strategic importance to the UK audit market. The firm has now experienced five consecutive years of recurring findings in key areas, indicating that previous quality improvement initiatives have not been sufficiently effective.

In response to these findings, the FRC has emphasized an urgent need for BDO to address the causes of its decline and implement a comprehensive quality improvement plan. BDO has committed to improving and has invested significantly in its audit practice. The firm has developed an audit quality transformation plan, implemented an engagement-level remediation program for in-flight PIE audits, and initiated a ‘Standback Review’ led by the Senior Partner to identify key factors impacting audit quality. An Actions Committee has also been established to ensure targeted and effective quality improvement measures.

A critical issue highlighted in the report is BDO’s admission that it was not able to fully implement an effective System of Quality Management (SoQM) as required by ISQM (UK) 1. In response, the firm has devised a remediation plan to redesign its system, investing in additional specialists to systematically review and enhance the SoQM design. This is a crucial step, as an effective SoQM is fundamental to consistent, high-quality audits.

BDO now faces the immediate challenge of reversing its decline in audit quality while maintaining its market position. The firm must effectively implement its SoQM remediation plan, address recurring findings through targeted interventions, improve its root cause analysis, and enhance its approach to complex areas such as estimates, impairment, and group audits.

The struggles faced by BDO highlight the challenges experienced by firms outside the “Big Four” in maintaining consistent audit quality. This situation underscores the importance of ongoing investment in quality processes and the potential need for increased support for mid-tier firms to ensure a diverse and resilient audit market.

The FRC has indicated that it may take stronger action, potentially including using its PIE Auditor Registration powers, if significant improvements are not seen in 2025. This puts considerable pressure on BDO to rapidly and effectively address its audit quality issues. The coming year will be critical for BDO as it strives to implement its improvement plans and demonstrate a meaningful turnaround in its audit quality performance.

Read BDO’s full report here: BDO_LLP_Audit_Quality_Inspection_and_Supervision_Report_2024

Forvis Mazars’ performance in the 2024 FRC review has raised significant concerns, with only 44% of its audits categorized as good or requiring limited improvements. This represents a decline from 56% in the previous year, placing Forvis Mazars in a position requiring substantial improvement among Tier 1 firms. Of the nine audits inspected, one (11%) was found to require significant improvements.

The firm’s performance shows a negative trend, partially reversing the improvement seen between 2021/22 and 2022/23. This decline is particularly concerning given Forvis Mazars’ strategic importance to the UK audit market. The firm has experienced recurring findings over the last two years in key areas, indicating that previous quality improvement initiatives have not been sufficiently effective.

FRC Recommendations and Firm Response

The FRC has emphasised an urgent need for Forvis Mazars to address the causes of its decline and implement a comprehensive quality improvement plan. In response, Forvis Mazars has taken several significant steps.

The firm developed an Audit Quality Transformation Plan (AQTP), introduced in October 2023, demonstrating its commitment to improving and investing substantially in its audit practice. To address points raised by the FRC, Forvis Mazars created a dedicated System of Quality Management (SoQM) team.

Additionally, the firm implemented a portfolio risk assessment to identify and mitigate risks related to specific audits or areas of concern. Furthermore, Forvis Mazars redesigned its in-flight review programme for 2023-24, incorporating full and focused scope reviews, follow-up reviews, and thematic reviews.

Forvis Mazars has implemented ISQM (UK) 1 and completed its first annual evaluation. However, the FRC noted that the firm needs to significantly enhance the evidencing and monitoring of its SoQM, and the extent of support for its annual evaluation process.

Forvis Mazars faces the immediate challenge of reversing its decline in audit quality while maintaining its market position. The firm must:

The FRC has indicated that it may take stronger action, potentially including using its PIE Auditor Registration powers, if significant improvements are not seen in 2025. This puts considerable pressure on Forvis Mazars to rapidly and effectively address its audit quality issues.

Read Forvis Mazar’s full report here: Forvis_Mazars_LLP_Audit_Quality_Inspection_and_Supervision_Report_2024