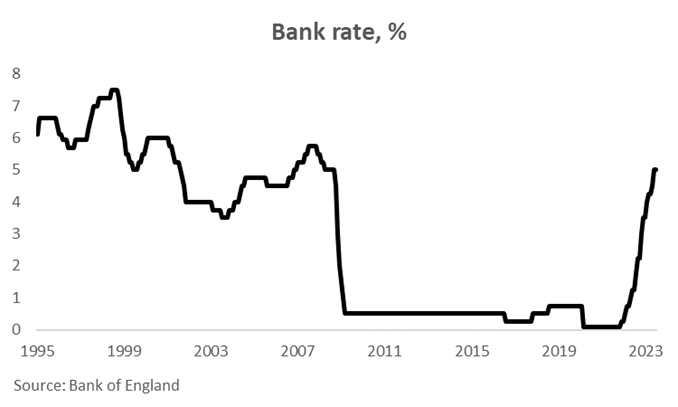

The Bank of England (BoE) raised interest rates by a quarter-point to 5.25% at its August meeting. This was the fourteenth consecutive increase in the current tightening cycle beginning in December 2021, and took rates to their highest level since early 2008 (Chart 1).

There was a three-way split on the Monetary Policy Committee (MPC). Six members voted for the quarter-point rise, two for a larger half-point hike, while the dovish Swati Dhingra continued to opt for unchanged policy. The new member, Megan Greene, agreed with the majority, confirming suspicions that she will be more hawkish than her predecessor, Silvana Tenreyro, who had been voting for unchanged policy since rates reached 3% in November.

Since surprising financial markets with the larger than expected half-point rate hike in June, this was the first meeting in which the MPC published its in-depth quarterly Monetary Policy Report and new economic forecasts, as well as holding a press conference to explain its latest thinking. These meetings are scrutinized especially closely by economists and investors, as they can be important for signalling the committee’s future intentions.

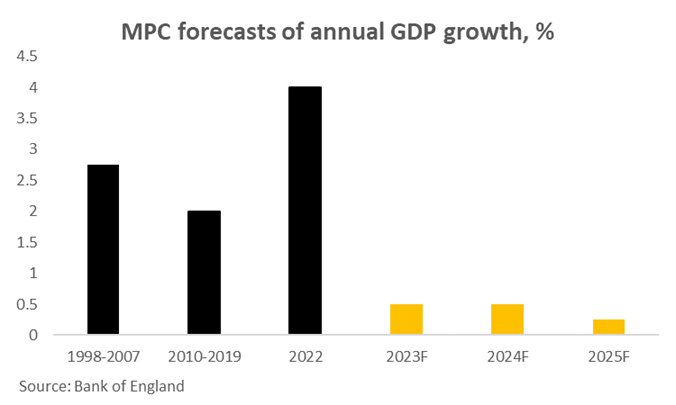

Given the economy’s recent resilience, the MPC has become slightly less pessimistic on GDP growth this year, expecting an expansion of 0.5%. It lowered its forecasts for coming years though, expecting growth of just 0.5% in 2024 and 0.25% in 2025 (Chart 2), compared with 0.75% for both previously. The driver of the downward revisions was the much higher expected future path for market interest rates since it made its previous forecasts in May. The committee is not expecting a recession, but growth is set to remain exceptionally weak by historical standards. The unemployment rate is forecast to rise from 4% currently, to 4.5% and 4.8% in the fourth quarters of 2024 and 2025.

Most attention is paid to the projections for inflation, as they provide an indication on how the MPC may see the future path for interest rates. Based on a market profile of rates rising to a peak of just over 6% and averaging just under 5.5% over the forecast horizon to 2026Q3, the MPC sees inflation around its target two years out and below in three years’ time (Chart 3). The committee’s forecasts are very similar if it assumes a profile of unchanged interest rates at 5.25% throughout the period.

The glass half-full inference from these projections is that the MPC doesn’t appear to envisage much, if any, further monetary tightening being necessary to get inflation back to its 2% target. Indeed, Governor Bailey suggested in the press conference that there was no presumed future path for rates, and stressed that both the market and unchanged profiles for interest rates return inflation to target.

However, a glass half-empty takeaway is that to achieve its targets the MPC envisages interest rates remaining elevated for an extended period, disappointing those hoping for a material cut in rates next year. It reinforced this message in the meeting minutes, suggesting the current monetary stance is ‘restrictive’ and that ‘The MPC will ensure that Bank Rate is sufficiently restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term, in line with its remit’.

The MPC has clearly chosen to maintain flexibility on what it may do next, with further monetary tightening depending heavily on data developments. With policy now judged to be in restrictive territory, the committee clearly sees risks from both insufficient and excessive tightening.

Key focus will be on measures of inflation persistence and the activity data. Services inflation, labour market strength, and wage growth will be particularly closely watched. Regular pay is growing at a record pace, which is contributing to very high service price inflation. Some forward-looking indicators point to a cooling in the labour market and pay growth, but the MPC will need to see clear evidence of this occurring before calling time on rate hikes. In terms of activity, if growth were to slow by more than expected in coming months, that could provide more leeway for the MPC to keep policy on hold, as it would result in some additional easing in labour market conditions and underlying inflation pressures.

All in all, developments on the inflation front are beginning to look at bit more auspicious for the inhabitants of Threadneedle Street. Headline inflation fell sharply in June, and the MPC is becoming more confident that it will fall back to around 5% in the fourth quarter, primarily due to lower energy inflation. The marked declines in inflation evident in the US and euro area are also providing encouragement.

Nevertheless, with underlying measures of inflation still very elevated and growth likely to continue to show some resilience, I still suspect that some further monetary tightening will be needed over the remainder of the year, although a peak in rates below 6% is beginning to look increasingly likely. But don’t cheer too loudly, because a long period of feeble growth and high interest rates looks set to be the order of the day. Accountants should advise their clients to plan accordingly.