Accounting professionals signal slowing global growth

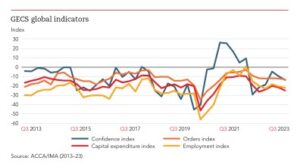

The latest survey for the third quarter recorded a second consecutive decline in ‘Confidence’ at the global level

The latest survey for the third quarter recorded a second consecutive decline in ‘Confidence’ at the global level

Every quarter, ACCA (the Association of Chartered Certified Accountants) and IMA (Institute of Management Accountants) survey Accountants, Auditors, Directors, Managers and CFOs from across the world on how economic conditions are impacting their firms or clients. Our Global Economic Conditions Survey (GECS) has been running since 2011 and provides invaluable on-the-ground insights from a diverse group of accountancy and finance professionals.

The latest survey for the third quarter recorded a second consecutive decline in ‘Confidence’ at the global level (see Chart 1), although sentiment is only slightly below its long-term average. There were also modest declines in the other key indices – ‘New Orders’, ‘Employment’ and ‘Capital expenditure’. New orders are in line with their average, employment is slightly above, while capital expenditure is moderately below. The narrative would seem to be one of a global economy that is slowing, but there is little evidence to suggest that a material downturn is imminent.

A cross-check on our economic indicators is provided by our GECS ‘fear’ indices, which reflect survey respondents’ concerns that their customers and/or suppliers may go out of business (see Chart 2). At the present time, there appears to be surprisingly little fear evident amongst accountants globally. Concerns about customers going out of business ticked up slightly, but fears about suppliers declined again. Neither series looks particularly worrying by historical standards. That said, given that monetary policy tightening works with lags, and government bond yields have risen sharply since the summer, some deterioration in these indices would seem highly likely over coming quarters.

Turning to prices, the sharp falls in headline inflation in most countries over recent quarters has been encouraging, as have declines in core inflation. However, with service sector inflation remaining at elevated levels in many countries, it would appear premature for central banks to declare victory in their battle against inflation. That is certainly the message coming from accountants. Concerns globally about costs eased again in the latest quarter but remain elevated by historical standards (see Chart 3).

On a regional basis, there was a notable reduction in confidence in North America of almost twenty points (see Chart 4), which comes on the back of four consecutive quarterly gains previously. The decline for the U.S. of nine points was not quite as marked as that of the broader region, but suggests that the first cracks could be beginning to appear in the previously resilient U.S. economy. Indeed, after expanding by almost 5% at an annual rate in Q3, growth is likely to significantly slow over coming quarters. Some of this will reflect payback from the very strong Q3 growth, but it will also be the result of various headwinds, such as the lagged impact of past monetary tightening and the sharp spike in government bond yields over recent months (see Chart 5).

Elsewhere, there was a modest rise in confidence in Asia Pacific, which came on the back of a very sharp decline in the previous quarter. Signs that gradual policy easing may be leading to a tentative recovery in the Chinese economy could have driven the stabilisation in confidence in the region. Confidence fell again in Western Europe, which is not surprising given that the Eurozone economy moved into contractionary territory in Q3.

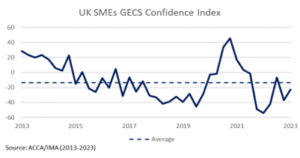

Closer to home, confidence improved slightly among UK small and medium-sized enterprises (SMEs) after a sharp decline previously, but sentiment remains below its average (see Chart 6). The New Orders Index was largely unchanged. But the indices for capital expenditure and employment point to growing caution on behalf of SMEs, with the former dramatically below its average (see Chart 7). The index measuring SMEs investment in their staff is also quite depressed by historical standards. With interest rates at their highest since 2008 and the UK economy at significant risk of contracting at the present time, a difficult winter lies ahead for SMEs.

All in all, the GECS survey remains consistent with some further loss in global economic momentum, although it does not suggest that a major downturn is imminent. That said, the risks to global growth are heavily stacked to the downside. These risks include the lagged impact of past monetary tightening, soaring government bond yields, geopolitics and oil prices, and the Chinese economy. Accountants and CFOs should hope for the best, but be prepared for the worst.