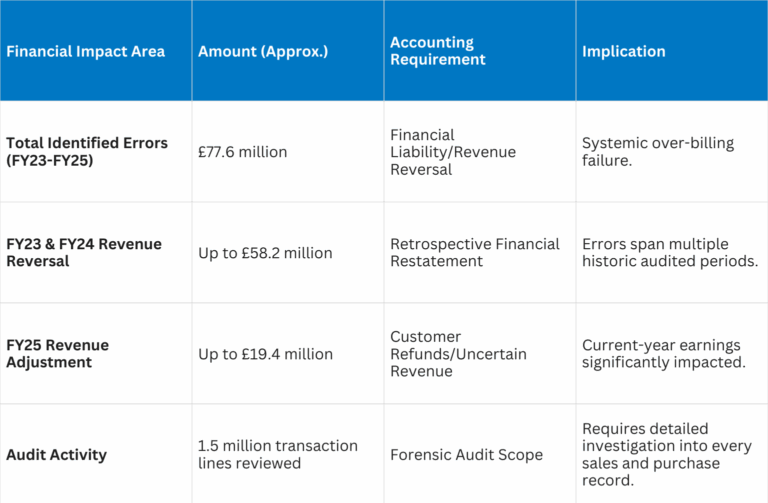

The colossal £77.6 million accounting blunder at Corporate Travel Management (CTM), now subject to an urgent UK Government investigation, serves as a stark and immediate lesson for every UK accountant on the catastrophic consequences of control failures. This is no mere timing difference; it is a restatement of revenue that cuts across public trust, corporate governance, and the financial integrity of public sector procurement.

The Anatomy of the Accounting Failure

The crisis originated in the Australian-headquartered travel management company’s UK and European division, specifically involving overcharges to a “small number” of UK-based customers, including the sensitive contracts held with the UK Home Office.

Key Financial Data Points:

The core of the issue, according to industry speculation and analyst reports, appears to be a failure in the reconciliation of refunds. It is suspected that when flights or services were cancelled, the refund received by CTM (as the booking agent) from the airline was allegedly not systematically passed back to the client, but instead recorded, or retained, as revenue. This failure speaks directly to a breakdown in fundamental cash control and revenue recognition practices.

The Government and Public Accountability Crisis

The involvement of the Home Office, a significant CTM client through the Crown Commercial Services (CCS) frameworks, elevates the matter from a corporate scandal to a crisis of public financial management.

The Home Office confirmed an “urgent investigation is underway” and has vowed that “All taxpayer money owed will be recovered.” CTM’s responsibilities included arranging contingency accommodation for asylum seekers, including the controversial Bibby Stockholm barge project. The overcharging of public money, especially in a politically sensitive area, puts intense pressure on government finance teams.

Implications for Public Sector Financial Teams:

-

Contractual Rigour: The Home Office, and by extension the CCS, will be forced to implement significantly stricter financial audit rights and performance metrics in future contracts. The focus will be on mandated, independent, and frequent checks on refund reconciliation and billing against source documents.

-

Due Diligence: Accountants involved in public sector procurement must now demand a higher level of financial transparency and governance assurance from third-party suppliers, going beyond standard annual accounts.

The Lessons for UK Accountants: Audit, Governance, and Control

The CTM case provides a live, three-pronged warning that must be internalised by every finance director, financial controller, and auditor across the UK:

1. The Failure of Internal Controls: The ‘Hidden Liability’

The errors went undetected for at least three fiscal years (FY23–FY25) before being flagged by the new auditor, Deloitte, prompting CTM to engage KPMG for a forensic review.

-

Action Point for Financial Controllers (FCs): This demonstrates the danger of a fragmented or weak revenue reconciliation process. For any business acting as an agent (an intermediary between a supplier and a customer), the distinction between gross revenue (total transaction value) and net commission/fee revenue (the actual income) is paramount. If client money (like a refund) is incorrectly treated as the company’s revenue, the formula for revenue recognition under IFRS 15 fails completely.

-

Preventative Measure: Implement a zero-tolerance reconciliation policy for any client funds, where any aged debtor balance or unreturned client cash must be flagged to an independent authority (e.g., the Audit Committee or Global CFO) within a set deadline (e.g., 30 days).

2. Governance and Oversight Collapse

The scale of the restatement led to the temporary suspension of the CTM UK & Europe Chief Executive and triggered an external governance review. This confirms that the fault lies not just in a system, but in the oversight culture.

-

Action Point for Audit Committees/Boards: Auditors must now actively question why a systemic issue of this magnitude was not detected internally. The case highlights that even routine, high-volume transactions, like processing travel refunds must be subject to independent review cycles as a key financial control, not just a back-office operation. The absence of effective whistleblowing or internal checks against client complaints allowed the issue to metastasise.

3. The Forensic Audit Mandate

KPMG’s draft report, which involved sifting through 47,000 documents and 1.5 million transaction lines, demonstrated the level of effort required to unpick the mess. Critically, KPMG also flagged a further £45.4 million in revenue from concluded contracts (2021–2023) as an “area of concern”, suggesting the final liability could grow further.

-

Lesson for Auditors: This reinforces the necessity of professional scepticism when auditing complex, high-volume transactions, particularly in agency-based businesses. The primary audit focus must be on the flow of cash that does not belong to the company i.e., client money held in trust accounts or money due back to clients. The distinction between an accounting error (unintentional misapplication of principles) and fraud (intentional misstatement) is now the central question for the forensic team.

The CTM crisis serves as a non-negotiable reminder: robust financial controls are the bedrock of trust, not just compliance. When controls fail, the financial fallout can be swift, material, and severely damaging to reputation and taxpayer confidence.