Confidence among global accountants rises again in Q2 2024, despite a big drop in sentiment in the US

The ACCA and IMA Global Economic Conditions Survey (GECS) suggests that global confidence among accountants and finance professionals improved slightly in Q2 2024 and is just above its historical average. There were also small gains in the Capital Expenditure, Employment, and New Orders indices (see Chart 1). The first is slightly below its average, while the latter two are slightly above average.

The latest survey results also revealed growing optimism among chief financial officers (CFOs) in our panel. All the key indicators for CFOs rose, with sharp gains in the New Orders and Capital Expenditure indices.

The picture was somewhat mixed at the regional level (see Chart 2). Confidence among accountants registered another decent increase in Western Europe, consistent with continued recovery in the euro area and UK economies. There was also a small rise in confidence in Asia Pacific, which came after a huge gain previously, and a marked increase in the New Orders Index. The region is benefitting from improvements in the global economy, including the manufacturing sector and technology cycle.

By contrast, there was a sharp fall in confidence in North America, which was even more pronounced for the U.S. The U.S. economy has slowed from the heady pace of expansion in the second half of 2023, and the latest results raise the risk of some further moderation over coming quarters.

The probability that the U.S. Federal Reserve begins easing monetary policy after the summer has increased, although inflation developments over coming months will be crucial. Changes in monetary policy by the Federal Reserve have major global ramifications. The beginning of rate cuts would ease global financial conditions and reduce the currency depreciation pressures that many countries currently face.

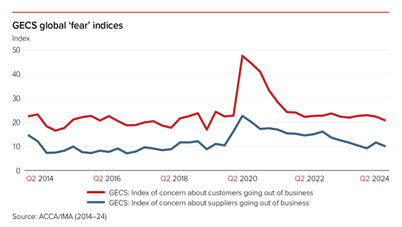

Meanwhile, our early indicators of corporate stress don’t look worrying at the present time. Our global ‘fear’ indices, which reflect respondents’ concerns that customers and/or suppliers may go out of business, both eased in the latest quarter (see Chart 3), as did global problems accessing finance and securing prompt payment.

Turning to inflation, global concerns about increased operating costs eased slightly but remain elevated by historical standards. Cost pressures remain elevated in all regions, except for the Middle East. This suggests that those central banks enacting, or contemplating, monetary easing need to tread very carefully.

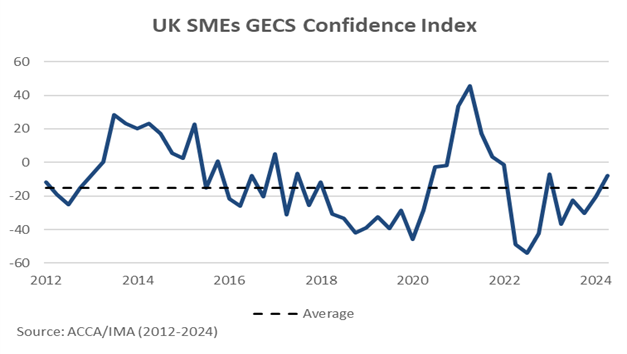

Looking at UK small and medium-sized enterprises (SMEs), confidence improved again in the latest quarter, consistent with the ongoing recovery in the UK economy (see Chart 4). Nevertheless, the picture from the other key indicators was mixed. The Employment Index improved, but there was a very sharp decline in the Capital Expenditure Index, perhaps reflecting uncertainty related to the election, and the New Orders Index also declined. This would suggest that the recovery may not be on particularly firm ground at the present time. A likely pivot to monetary easing by the Bank of England in coming months should prove helpful though. Financial markets are expecting at least one rate cut by year end.

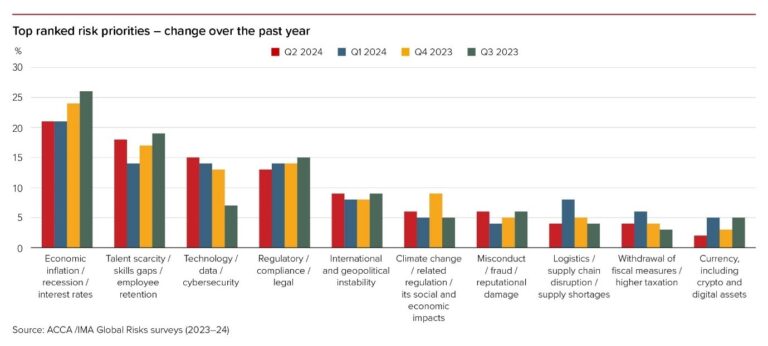

In our quarterly GECS, we also ask accountants to rank their top three risk priorities at the present time (see Chart 5). Economic-related risks remain in first place, but for the first time in a year, it is not the top concern for respondents working in financial services, although it is close to the highest it has ever been for those in the corporate sector.

Responses to the question, ‘what is the most underestimated risk?’, suggest leaders are increasingly struggling to navigate their organisations through the accumulating waves of uncertainty this year, particularly when it comes to cybersecurity which ranks as the third highest risk priority for all sectors combined.

In summary, the GECS points to some further improvement in the global economy in Q2. Further signs of a pickup in the important Western European and Asia Pacific regions are encouraging, but the decline in the North American and U.S. indices bear watching closely.

Meanwhile, despite the resilience of the global economy so far in 2024, many important downside risks and challenges remain. Sticky inflation could limit central banks’ scope for monetary easing, while geopolitical and political risks remain very elevated and will continue to create significant uncertainty.