How to lose £9bn a year without even noticing

UK SMEs are missing out on billions in savings interest, not because of economic volatility or poor decision-making, but because they’re parked with the wrong bank.

That’s the stark takeaway from new data released by Allica Bank, whose ongoing tracking of business savings rates has revealed a growing chasm between what challenger banks and traditional high street banks are offering to SMEs.

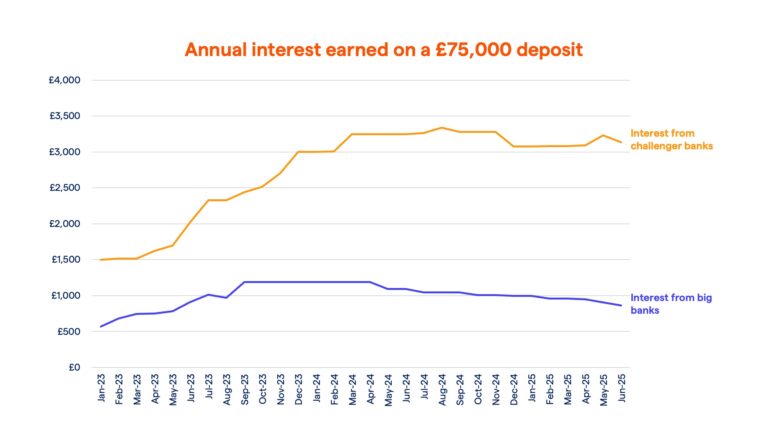

In May 2025, the average small business with £75,000 in savings earned £906 in interest from a Big Bank. The same sum deposited with a challenger bank would have generated £3,232 — a difference of over £2,300.

For businesses with seven-figure reserves, that discrepancy runs into the tens of thousands. And yet, despite years of base rate fluctuations, the inertia in SME banking relationships has remained largely unchanged.

“It’s so disappointing to see the way Big Banks continue to provide such poor value to their SME customers,” said Richard Davies, CEO of Allica Bank.

“At the start of 2023 there was already a significant gap… but it’s clear from the trend… that Big Banks do not prioritise their SME customers.”

Allica’s figures are not based on cherry-picked case studies or theoretical comparisons. Using Moneyfacts data and its own methodology, the bank has tracked savings rates offered to SMEs by the UK’s six largest banks — Barclays, HSBC, Lloyds, NatWest, Nationwide, and Santander — since early 2023.

According to its June 2025 tracker, the average SME is now losing £2,274 per year by sticking with the major players.

For accounting firms, the findings pose an uncomfortable question: are clients being properly advised on the cost of complacency? As interest rates rise and fall, cash management has become more than just a treasury concern.

“This latest data from Allica is a wake-up call for businesses to reassess whether they’re making the most of any excess cash sitting in their accounts,” said Claire Burden, Partner and Head of Consulting at S&W.

“Smart cash management has once again become a powerful tool for businesses… It’s an opportunity we haven’t seen on this scale since before the 2008 financial crisis.”

There are 5.5 million SMEs in the UK. Allica estimates that the cumulative shortfall in potential interest earnings across the segment amounts to £9 billion per year.

That’s capital which could be reinvested in hiring, automation, expansion — or simply absorbing the rising cost of doing business.

While challenger banks have held SME interest rates above 4% for much of the past two years, the big banks’ average offering has hovered between 0.76% and 1.59%.

Even with the Bank of England Base Rate falling to 4.25% this year, the gap in returns — now at 3.03% — shows no sign of closing.

According to Allica’s report, a business with £1 million in savings would have earned £42,000 in annual interest with a top challenger bank in June 2025, compared to just £12,000 from a high street bank.

The margin — £30,000 — is not insignificant, particularly for firms managing tight margins or planning for investment.

While the discrepancy in interest rates might appear as a technical detail, it reveals a deeper market inefficiency.

Despite increased regulatory attention on consumer savings products in recent years, the SME segment remains largely unexamined.

Unlike individual savers, small businesses are not routinely prompted to review their options or switch providers.

The result is inertia — and in this case, inertia with measurable cost.

The data suggests a policy blind spot: if the aim is to improve productivity, support growth, and enable businesses to weather economic volatility, then better visibility and access to competitive savings options may be an overlooked lever.