As we move through March, the dust has finally settled on Chancellor Rachel Reeves’s latest Spring Statement. For those of us in the profession, the takeaway was clear: “stability over surprises.” While the headline speech may have lacked the dramatic “rabbit out of the hat” moments of Chancellors past, the implications for UK accountants are profound, particularly as we approach the final weeks before implementation to the most significant shift in the personal tax regime in a generation.

With Making Tax Digital for Income Tax Self-Assessment (MTD ITSA) now just weeks away, the “wait and see” period is officially over. Here is our analysis of how the Spring Statement and the latest HMRC updates are reshaping the landscape for your practice and your clients.

MTD ITSA: No More Delays in the “Last Chance Saloon”

There was a quiet hope among some segments of the profession that the Chancellor might use the Spring Statement to announce a further deferral for MTD ITSA, citing the ongoing economic volatility or software readiness. However, that “last chance saloon” has now closed.

The Government has reaffirmed the 6 April 2026 start date. Crucially, the thresholds remain fixed, but the net is widening. The current roadmap is:

-

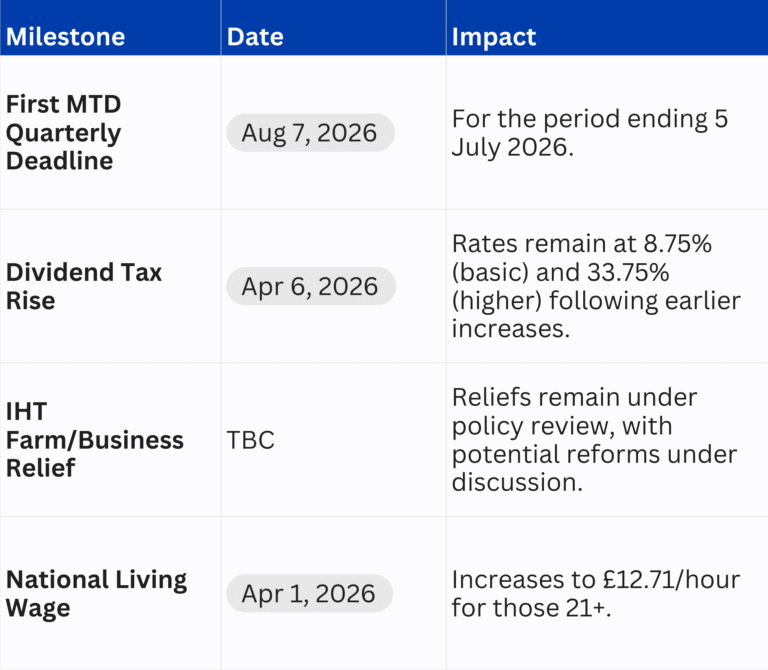

April 2026: Self-employed individuals and landlords with qualifying income over £50,000.

-

April 2027: Those with income over £30,000.

-

April 2028: The threshold drops to £20,000 (as clarified in recent policy updates).

The “Qualifying Income” Trap

It is vital to remind clients that the threshold is based on gross income (turnover), not profit. We are already seeing “Case Study A” scenarios in practices across the UK: a consultant with £55,000 in revenue but high expenses, leaving them with a modest £25,000 profit might assume they are under the radar. They are not. If their most recent 2024/25 return shows gross income above £50,000, they are in Phase One.

The Spring Statement: Fiscal Drag and the Advisory Opportunity

While the Chancellor avoided major tax hikes, the decision to maintain the extended freeze on thresholds, currently set through April 2028, with continued fiscal drag expected beyond.

As inflation-driven wage growth continues, more of your clients will be pushed into higher tax bands. For accountants, this moves the needle from “compliance” to “proactive wealth protection.”

-

Dividend Tax: With the basic and higher rates on dividends rising, the Spring Statement’s silence on further changes actually provides a clear window for planning.

-

Case Example: Consider a director-shareholder of a small LTD. With the Corporation Tax main rate held and dividend taxes rising, the “salary vs. dividend” conversation for the 2026/27 tax year needs to happen now, not next March.

HMRC’s “Soft Landing” on Penalties

A significant update for practitioners this month is the clarification on the points-based penalty system. HMRC has confirmed that they will not apply penalty points for late quarterly updates during the first year of mandation (2026–27).

However, and this is a big “however” this is not a free pass. Penalties for late payment of the actual tax bill and late filing of the Final Declaration will still apply. This “soft landing” only applies to the quarterly summaries. Our advice? Don’t let your clients treat this as a holiday. Use the first year to bake in the habit of quarterly reporting without the fear of a £200 fine hanging over every 7th of the month.

Practice Management: The Digital “Squeeze”

The Spring Statement’s focus on UK productivity growth (forecast to rise to 1% in the medium term) mirrors the challenge within our own firms. The “digital squeeze” is real. Transitioning a portfolio of 200 landlords from annual “shoebox” accounting to quarterly digital submissions is a massive operational lift.

We are seeing a trend where firms are categorizing clients into “Digital Ready,” “Digital Reluctant,” and “Digitally Excluded.”

-

Digital Ready: Already on Xero/QuickBooks focus on refining their categorization.

-

Digital Reluctant: Still on spreadsheets introduce “bridging software” as a middle-ground solution.

-

Digitally Excluded: Note the latest HMRC guidance (updated Jan 2026) regarding exemptions for age, disability, or location. The bar is high, and applications for exemption should be started sooner rather than later.

The Deadlines That Will Define Your Next 12 Months

The Accountancy Age View

The 2026 Spring Statement confirmed that the Government is staying the course. For accountants, “staying the course” means accelerating the digital transition. We aren’t just tax preparers anymore; we are transition managers.

The next few weeks should be spent auditing your client list against the 2024/25 tax year figures. If you wait until the filing deadline to tell a client they need to be MTD-compliant by April, you’ll be facing a bottleneck that no amount of overtime will fix.